Banks in Southeast Asia rely on retail branches to serve existing customers and bring in new ones. Since the COVID-19 pandemic began, banks have scaled down their branch networks to protect their employees, comply with local restrictions, and simplify logistics like cash collection. At the same time, retail and corporate customers are counting on digital banking services more than ever. How are banks addressing the sudden change in demand?

Digital-ready banks are seeing a significant increase in new sign-ups, most at a rate of more than double the average registrations. In the Philippines, Rizal Commercial Banking Corporation (RCBC) reported a 259% increase in new online accounts within the first three days of enhanced community quarantine; UnionBank in March opened 7,000 new accounts and had 20,000 downloads of its app in March, with website traffic doubling.

Likewise, corporate clients face new banking challenges now that branches and their offices are closed. Check printing, paper-based approvals, and branch-based transactions now need to come online. For instance, many corporations in the region are struggling to approve, process, and track supplier payments; corporate online banking portals are complicated, slow, and typically require weeks to set up and customize. During these abnormal times, it may take months for a traditional bank to enable corporate banking access to a new user.

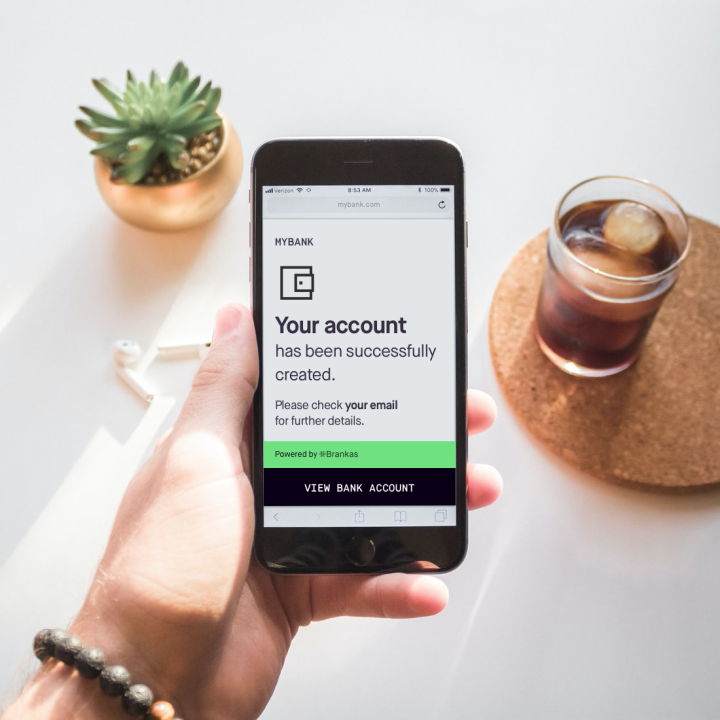

Brankas is partnering with banks across the region to fast-track technology partnerships for retail and corporate banking. We have developed new account opening APIs, making the customer onboarding process as easy as possible. Account opening APIs allow the bank to acquire new customers through third-party channels, typically non-bank financial services providers like remittance centers, ecommerce marketplaces, and loyalty programs. The service can enable new checking/savings account signups, as well as credit cards and loan origination. Brankas is able to offer a more cost-effective plug and play technology to move branch account openings online, rather than having to build the same technology in-house. In addition, Brankas can set-up interbank direct debit transaction capabilities and provide a top-up mechanism to fund the account from other bank accounts.

Regulators are ensuring customers have access to financial services and are supportive of this online shift. In the Philippines, banks have until June 30th, 2020 to avail of the temporary relaxation of KYC rules, subject to a few qualifications by the Central Bank. In Indonesia, BI has also declared simplified requirements to the online account application process.

Brankas is a leader for Open Banking in Southeast Asia. Partnering with Brankas speeds up your transition to digital enabling you to move faster, create better products, and reach even more customers. Beyond the account opening use case, APIs are transforming the way banks do business and interact with customers enabling new channels and secure, scalable, and real-time digital products.