Open Banking in Indonesia: Unlocking New Fintech Opportunities

2017: A Blockbuster Year for FinTech

2017 was an important year for the Indonesian FinTech scene, with multiple strategic acquisitions, banks launching their first API-based financial products, and a matching increase in regulatory oversight. Gojek, a leading multi-service and digital payment technology company in Indonesia, acquired 3 FinTech firms - Kartuku, an offline payment processing company; Midtrans, one of the leading online payment gateways; and Mapan, a community-based savings and lending network. These acquisitions also worked to expand the reach of Gojek’s GoPay, a digital wallet launched in 2016. In the same year, the ride-hailing giant Grab acquired Kudo, a FinTech that aims to provide offline users the ability to buy online items through physical kiosks. Banks were also beginning to launch their own products using APIs, such as Bank Central Asia’s (BCA) OneLink, that helps users top up their GoPay wallets using their BCA accounts. In the same year, Indonesia’s Financial Services Authority (OJK) inaugurated a FinTech Advisory Forum, serving as a platform to set direction for FinTech development in the country – a culmination of all the growth FinTechs were experiencing in the region. The unprecedented rise in FinTechs and their popularity comes in part because of the nature of the Indonesian market. With a large unbanked population yet a high mobile penetration rate, digital banking has become a viable option in an effort to provide a larger portion of the population with modern financial services.

2020: A New Wave of FinTech led by Open Banking Technology

After a few years of significant growth in the FinTech industry, 2020 marked the beginning of a new wave of FinTech in the country led largely by Open Banking. More Open Banking initiatives began to emerge, stemming from collaboration between traditional banks and FinTechs. BCA partnered up with Shopee for an online payment solution, OneKlik, allowing customers to pay merchants instantly from within the Shopee app. This speeds up online transactions immensely whilst still ensuring security of users’ accounts. OJK also provides regulation on businesses relating to digital payments, securing data shared by users and ensuring that all digital payment platforms have been screened by OJK. In early 2020, Standard Chartered launched Nexus, its “Banking as a Service” solution that allows digital platforms to provide banking services to its customers under their own name. Tokopedia is also empowering its partner merchants with financing loans by partnering with banks, startups and eWallets, and leveraging merchants’ transaction data to speed up the loan approval process. The user can instantly compare loan rates and installment options among participating lenders. Once approved, the loan proceeds are disbursed directly into the merchant’s Tokopedia account. Despite these many advancements, it is still early on for Open Banking and it still faces many limitations. Specifically for small businesses, availing of these open banking services may be costly and time consuming, often making it difficult to successfully integrate these services into their businesses.

Taking into account these issues and barriers to use, an Open Banking platform that requires lower costs and convenient onboarding may be the answer – such as a platform like Brankas.

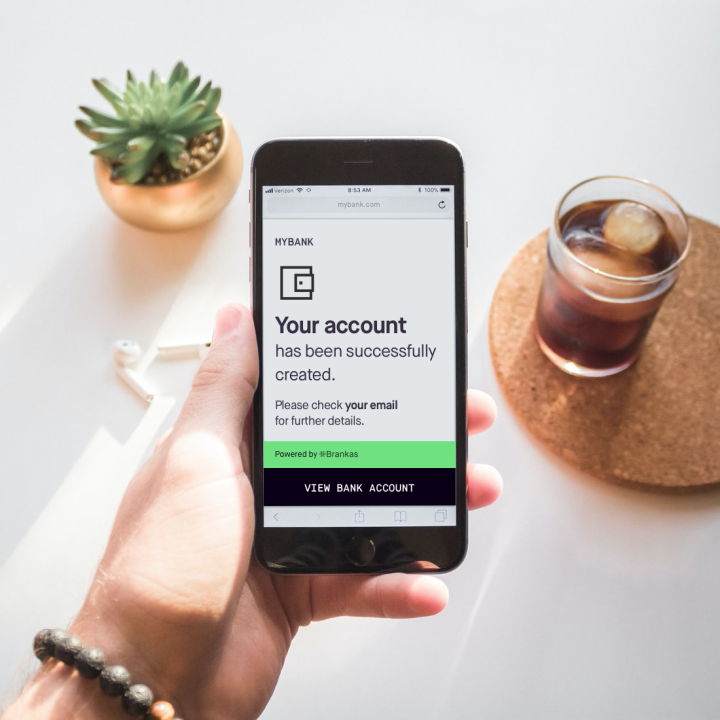

Introducing Brankas: Bringing Open Banking to Southeast Asia

Brankas offers low-cost, direct customer-to-merchant transaction options that require only a single integration to connect to multiple banks. Brankas also provides a highly secured network and lower transaction fees by eliminating the middleman. Brankas has three main API product offerings, which we can customize to fit the client’s particular use cases. If your business requires you to create a credit score, Statement can help by providing the user’s bank transaction history easily. If you are running a P2P lending business, Disburse lets you send money in bulk to multiple recipients that are using different banks with a single file upload. If you want to build a service similar to OneLink, Brankas can help make that happen with Direct, with only one integration to access all its partner banks.

Open Banking may be the key to unlocking the potential of technology to revolutionize the financial industry, but in order to truly do so, we must ensure that MSMEs are provided the same possibilities to leverage on these advancements. Today’s circumstances have highlighted the fact that more than ever, we need modern, accessible financial services that are able to serve the majority of the population. In recent years, there has been a push for tighter Open Banking regulations in Indonesia, and the government has unveiled the Indonesia Payment System Vision 2025 that opens up countless opportunities to weave Open Banking practices into the business model of many companies.There is a need to provide services that are accessible, low cost, and reliable, allowing any business to easily integrate technologically-reliant services into their platforms.

At Brankas, we can help you create financial technology tailor-fit to your business. Interested in learning more about us and our services? Check out our website.