The rise in technology has changed the way people perceive banks. They are no longer just physical buildings where people keep their hard-earned money. Nowadays, many banking customers identify financial institutions with an app or a website, allowing them to access their finances conveniently.

Indeed, digital transformation is necessary for banks and other similar firms. By using open-source API, banks can diverge from siloed data and update their infrastructure to adapt to modern times.

So what is open-source API, and how can it help the banking industry?

What is Open-Source API in Banking?

Before knowing how this programming term works in banking, it’s essential to understand what an API is. An application programming interface (API) acts as a bridge that helps two or more systems communicate. In other words, the API provides an easier and more secure passageway for information to travel from application to application.

An open-source API has cross-application integration capabilities. You can think of this API as a “plugin” that your system can use to access others.

Financial institutions can allow their partners to connect to their systems and access customer information via open banking API. This way, both parties can provide a seamless customer experience for payments, fund transfers, etc.

Last but not least, turning to open-source banking lets banks create innovative products that can attract more customers.

Why Should Banks Enable Open-Source APIs?

Like any business, banks need more customers to grow. To attract more clients, banks must offer the best customer experience. Allowing open-source APIs into banking systems can help them provide a broader range of services that consumers need.

But how exactly does open banking benefit the industry? Here’s what allowing open-source APIs into banking systems can achieve.

-

Meet consumer demand

Trends in consumer behavior constantly change. For example, the recent pandemic has made e-Commerce more popular than ever as consumers shop online. According to research, online retail sales may reach $6.51 trillion by 2023. With e-Commerce on the rise, it’s best to include online channels and e-wallets as payment options.

Here, open banking APIs fit the bill. Firstly, open-source APIs enable e-Commerce platforms to integrate a bank’s system, eliminating the need to log in to different applications.

Moreover, open-source banking allows for accessibility and convenience. Take, for example, going cashless through e-wallets. Open-source APIs like Brankas' Direct API lets users top up their e-wallets securely and quickly through bank transfer. As a result, customers can secure funds faster without physically visiting a bank.

-

Keep up with third-party providers

There’s no denying that the digital age is fast-paced. Technological advancements continue to increase, requiring companies to improve their processes and create an excellent customer experience. Third-party providers (TPPs) are no different.

However, traditional banks may be unable to keep up with TPPs at this pace. As such, using open-source API in banking can help banks and other financial institutions be on par with TPPs.

Moreover, giving TPPs access to primary customer data—with the client’s consent—cuts processing time for relevant transactions like loan applications.

For example, Brankas’ Statement API provides a comprehensive look into a customer’s financial data. With this feature, banks can share the necessary information with their partners and enable a quick, paperless, holistic credit risk assessment.

-

Ensure regulatory compliance

Cybercrime has increased along with internet usage. In fact, 2022 set a new record for the highest global average cost of a data breach at $4.35 million.

That said, governments have created policies to reduce cybercrime risk. For its part, the European Union (EU) enforces two regulatory policies that directly affect banking operations.

-

Payment Service Providers Directive (PSD2)

The PSD2 is a regulation that financial institutions and companies receiving electronic payments in the EU must adhere to. This regulation aims to improve consumer protection, foster competition, and innovate security in the payments sector. It also prompts concerned bodies to provide customer information to TPPs securely.

The regulation may not apply to companies and financial institutions outside the EU. However, those planning to expand to this region must comply with it.

-

General Data Protection Regulation (GDPR)

Investopedia defines GDPR as the “legal framework that sets guidelines for the collection and processing of personal information from individuals who live and outside the EU.” GDPR regulates the processing and usage of personal data that companies collect from consumers based on their internet activities.

Unlike the PSD2, the GDPR is a law that companies and banks must comply with if they want to continue serving EU citizens. This law applies regardless of where the firm is.

Ultimately, these EU rules can affect financial institutions entering the region. Banks can address similar regulatory compliance concerns with open-source banking solutions like Brankas' Open Core API. This solution helps banks and financial institutions comply with applicable data security regulations.

-

Enable banking-as-a-service opportunities

Open banking APIs have become a valuable asset for many financial services firms. Besides keeping up with partners, open-source APIs can give banks a competitive market edge. These APIs enable banks to enhance offers, improve customer engagement, and develop new digital revenue channels.

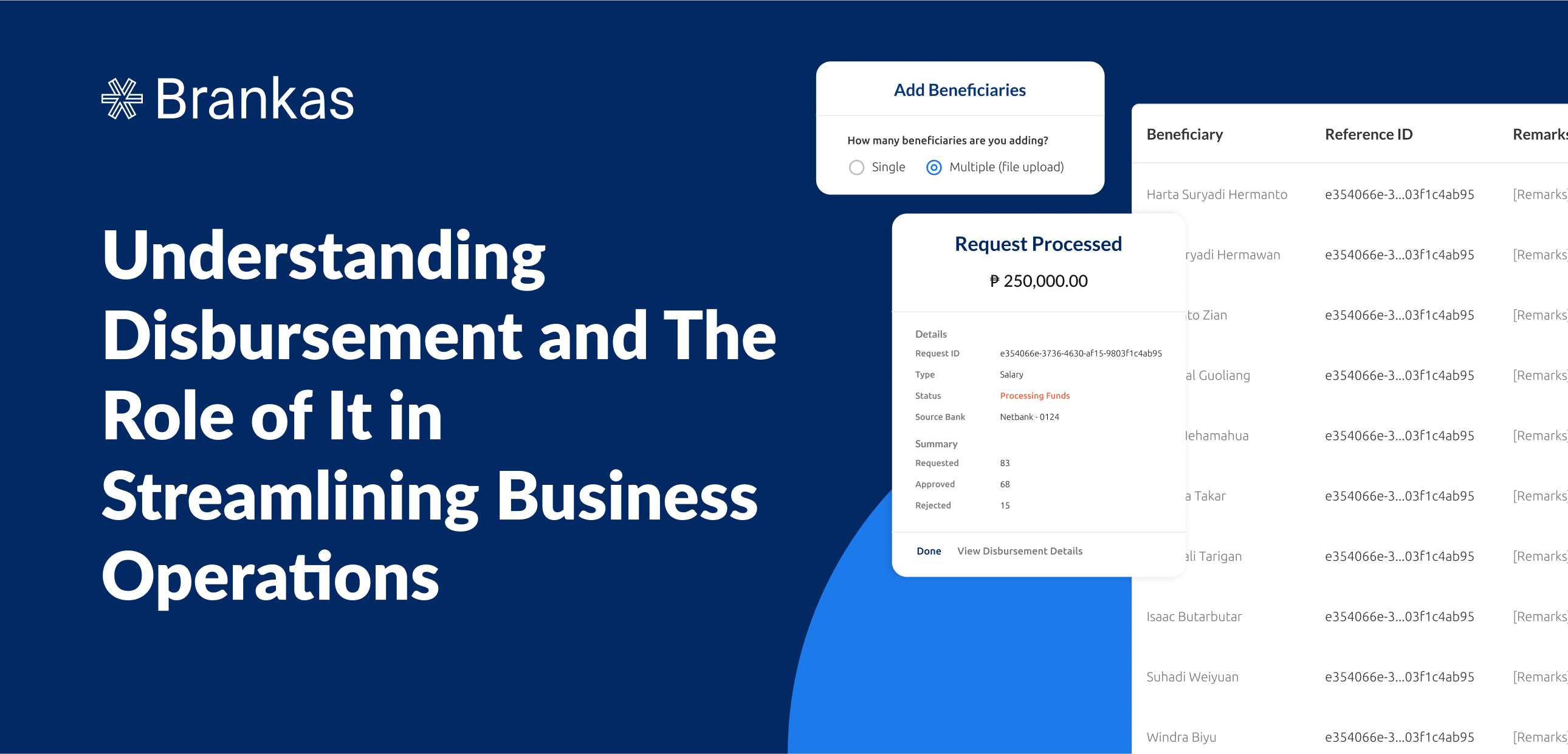

Moreover, banks can automate numerous processes through digital means, leveraging the benefits of banking-as-a-service APIs. These processes include account opening, payments, disbursements, cards, and loans. Doing so allows consumers to enjoy speedy financial services.

Additionally, solutions like Brankas' Open Finance Suite can give banks a secure plug-and-play gateway to extend their services to their partners. As a result, customers can connect to their core banking systems through their preferred partners.

The world’s thrust into the digital age has changed the nature of banking services. Thanks to open banking, customers can conveniently access their financial accounts.

Indeed, moving into the digital scene is a must. Through open-source APIs, financial institutions can adopt open banking and enhance the customer experience while staying secure.

Consider financial services providers like Brankas to move your bank forward in the digital world!